Process Improvement ROI: What to Expect at 30, 90, and 180 Days

- Maria Mor, CFE, MBA, PMP

- May 20

- 9 min read

You made the decision to fix the back office. You brought in outside expertise. You cleared time on your calendar and told your team something was changing.

Now you are waiting for proof it was worth it.

Table of Contents

That wait is where most process improvement engagements go wrong. The work is producing results, just not where business owners expect, or when they expect them. According to McKinsey, streamlining processes and tasks can result in an efficiency impact of 5 to 15 percent. Those gains are real. But they do not arrive on day one, and they do not announce themselves.

Revenue comes from the front office. Profit is protected in the back office. Understanding when and how that protection shows up on your income statement is what this post is about.

Why the Timeline Surprises Business Owners

Business owners who invest in process improvement want to see movement quickly. That instinct is reasonable. Most operational decisions in a growing company produce visible results within days.

Process improvement does not work that way. When a back office is losing profit, it is rarely because of one broken thing. It is because a series of undocumented, owner-dependent processes are each leaking a small amount. A slow invoicing cycle. A client onboarding that requires the owner to intervene every time. A hiring process that loses candidates because no one owns the follow-up. Individually, each looks manageable. Together, they quietly drain margin every single month.

Fixing this kind of structural problem follows a specific financial arc. The first phase removes the cause of the leak. The second phase makes the savings measurable. The third phase turns the fixed process into a compounding asset. Owners who understand this arc stay in the engagement long enough to capture the full return. Owners who do not often exit right before the numbers move.

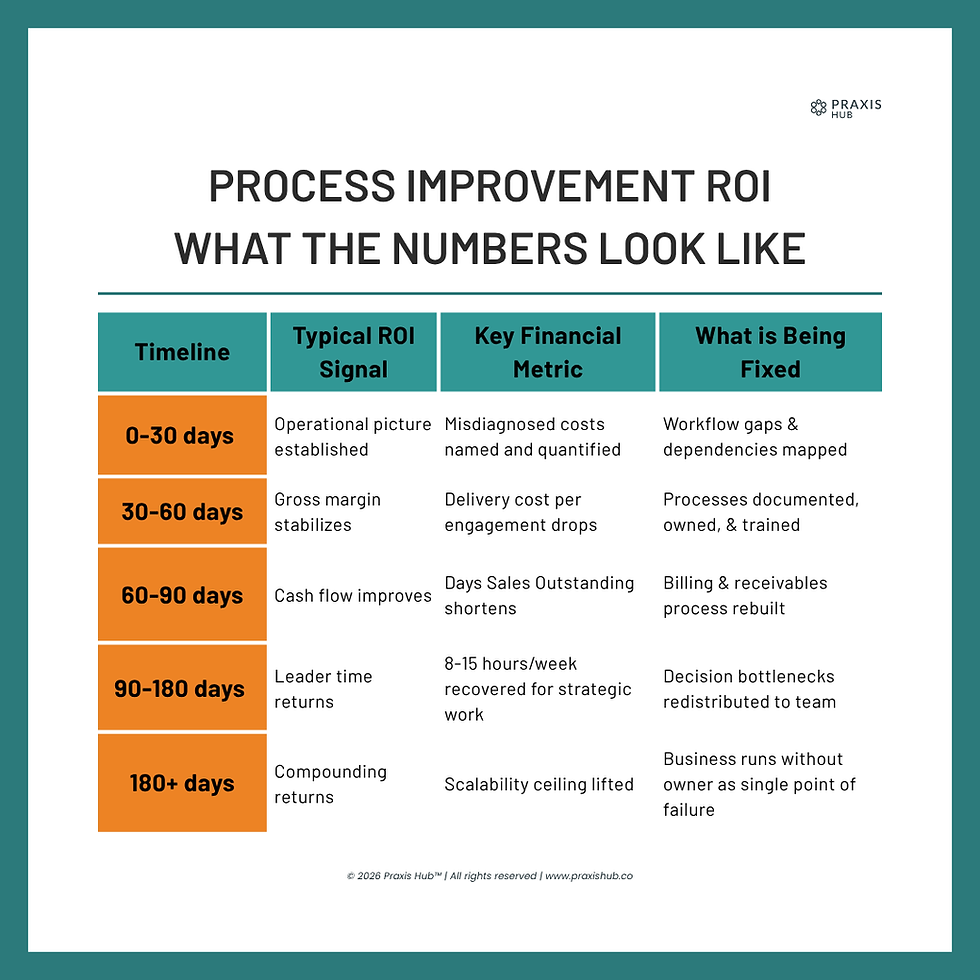

The First 30 Days: Stopping the Bleed

The first 30 days of a process improvement engagement produce something that does not appear on any report. They produce an accurate picture of what is actually wrong.

That may sound anticlimactic. It is not. In most businesses with more than ten employees, the owner's working theory about where the operational problems are is partially correct and partially wrong in ways that matter. Time gets spent on symptoms. The structural causes stay untouched. A business owner who believes the problem is in the sales handoff may discover the real issue is in delivery tracking three steps downstream. The financial leak is the same. The fix is completely different.

During this phase, the financial consequence being addressed is misdiagnosed cost. Decisions made on incomplete operational data create ongoing overhead that looks like a staffing problem or a revenue problem when it is neither. Once the actual processes are mapped and the gaps are documented, the cost finally has a name and a number.

What you should expect to see at 30 days: documented workflows across the highest-priority areas, a clear picture of where owner time is going and why, and a prioritized roadmap that sequences the fixes by financial impact. The ROI here is not visible yet in dollars. It is visible in the elimination of wrong assumptions, which is itself worth real money.

Before you consider adding any technology layer to your operation, this diagnostic phase is the work that must happen first. If you are evaluating whether your business is ready to systematize, this post on what to do before you automate your business covers the operational foundation required.

Days 30 to 60: Where the Numbers Begin to Move

This is where financial signals start to appear on the income statement. The fixed processes are running, the baseline from month one is established, and the difference is now measurable.

The most common early signal is gross margin stabilization. When delivery processes are undocumented, every client engagement costs slightly more than it should. Team members improvise. Owner involvement fills the gaps. Time that should be strategic gets consumed by process maintenance. Once workflows are documented, trained, and owned, delivery cost normalizes. The same revenue produces more margin.

The second signal is cash flow. Slow invoicing and inconsistent follow-up are back office problems with a direct line to the balance sheet. Days Sales Outstanding, the number of days between completing work and collecting payment, drops when the billing process is fixed and owned. A business bringing in $2 million annually and running a 35-day DSO is floating roughly $190,000 in receivables at any given time. Cutting that to 20 days frees nearly $90,000 in working capital without a single new sale.

The third signal, harder to quantify but equally real, is owner time returning to its highest use. When the bottlenecks that required owner decisions are redistributed with proper ownership structure, the business gains capacity without adding headcount.

What you should expect to see at 90 days: measurable reduction in delivery cost, shorter receivables cycles where billing was a known issue, and a reduction in decisions that can only be made by the owner. The Business Process Improvement services page outlines what this phase of engagement looks like in practice.

Days 60 to 180: Process Improvement ROI Compounds

The 90 to 180 day window is where the engagement pays for itself, often several times over. It is what happens when documented processes are fully adopted by the team and the owner is no longer the single point of failure for operational decisions.

A fixed process does not save money once. It saves money every time it runs. An onboarding process rebuilt to eliminate five owner touchpoints saves those hours with every new client. A month-end close shortened from 30 days to 5 days delivers accurate financial data 25 days earlier every single month. Decisions made on current data cost less than decisions made on 30-day-old data, and that difference accumulates.

In businesses where the owner has been functioning as the de facto operations manager, the return in this phase also shows up in recovered capacity. At $200 per hour of owner time, reclaiming 10 hours per week is worth roughly $100,000 annually. That is not a staffing decision. It is an operations decision.

The financial consequence being resolved here is scalability ceiling. Most businesses with 10 to 50 employees are not limited by demand. They are limited by the owner's personal bandwidth and the fragility of processes never designed to run without direct supervision. When those processes are fixed, documented, and team-owned, the ceiling lifts.

What you should expect to see at 180 days: the business can operate for one to two weeks without the owner as decision bottleneck, financial reporting is consistent and timely, and processes are functioning without exceptions or workarounds. The ROI shows up in margin, in working capital, and in the owner's ability to work on the business instead of in it.

What Determines How Fast You See Returns

The process improvement ROI timeline is not fixed. Several factors shape how quickly the financial results appear, and this pattern holds across industries and business models.

The first is operational clarity coming into the engagement. Businesses that have some documentation, even informal, give outside expertise a faster starting point. Businesses where every process exists only in the owner's head require more time in the diagnostic phase before implementation can begin.

The second is team readiness. Documented processes only produce ROI when the team follows them consistently. Business owners who communicate the change, explain the reason, and reinforce the new standard see faster adoption. Businesses where the owner introduces a new system but continues operating the old way create mixed signals that slow everything down.

The third is sequencing. Not all broken processes carry the same financial weight. Across different industries, the back office areas most likely to accelerate or delay ROI follow a recognizable pattern:

Billing and invoicing gaps that extend Days Sales Outstanding past 30 days

Delivery processes that require owner sign-off at multiple steps

Onboarding workflows that are never documented and restart from memory with every new client

Month-end close processes that run 2 to 3 weeks, delaying financial visibility

Approval chains where decisions sit until the owner responds

Engagements that prioritize these first, by income statement impact rather than visibility, produce measurable financial results earlier. If you want to understand where these gaps typically show up in a business like yours, this post on back office profit leaks covers the most common patterns and what they cost.

Why Outside Perspective Helps

There is a pattern that shows up consistently across industries. The processes that are costing the most are almost never the ones the owner identifies as the problem. They are the processes the owner stopped questioning years ago because they seemed to be working well enough.

This is a structural limitation, not a failure of attention. When you build a business from the ground up, you develop operational blindness to the systems you live inside every day. The gaps become invisible because everything around them has adjusted to compensate. The team works around the broken step. The owner fills in without realizing it. The cost accumulates silently.

Outside perspective backed by operational experience across different industries finds these patterns quickly. The advantage is structural, not intellectual: an outside advisor simply is not inside the system the way the owner is. The gap is never in what the owner knows. It is always in what the owner has stopped questioning.

Not Sure Where to Start? Take the System Leak Audit

The timeline described in this post is real, but where you enter it depends on what is actually happening in your back office today. The System Leak Audit covers five categories of back office profit drains and takes about 15 minutes. It is free.

Ready to Talk? Book a Discovery Call

A discovery call is a direct conversation about where your operation is losing profit and what a structured improvement engagement would address first. No framework pitch. No generic roadmap. A direct answer to the question your income statement is already asking.

Frequently Asked Questions

How long does process improvement ROI typically take to show up?

The first measurable financial signals typically appear between 60 and 90 days into a structured engagement. The first 30 days are primarily diagnostic: mapping workflows, identifying the true cost drivers, and documenting the baseline. Early indicators in the 30 to 90 day window include gross margin stabilization, shorter receivables cycles, and a reduction in owner-dependent decisions. Deeper returns, including the compounding value of consistently documented and team-owned processes, solidify in the 90 to 180 day range. Businesses with some existing documentation and a team that adopts new standards quickly tend to see returns earlier.

What financial metrics should I track to measure process improvement results?

The most direct indicators are gross margin, Days Sales Outstanding, and owner hours consumed by operational decisions. Gross margin shows whether delivery costs less per engagement once processes are standardized. DSO tracks how many days pass between completing work and collecting payment. Owner hours at your effective hourly rate quantify how much bottleneck time is costing the business. Establish baselines before the engagement begins and track at 30-day intervals.

Why do some process improvement engagements fail to produce ROI?

The most common reason is premature exit. Business owners who disengage after the diagnostic phase capture the cost of the engagement without capturing the return. A secondary cause is sequencing: fixing the most visible processes rather than the most financially impactful ones produces organizational activity without moving the income statement. A third cause is incomplete team adoption. Documented processes produce ROI only when the team follows them consistently, and owner behavior that contradicts the new standard signals the old method is still acceptable.

Can process improvement ROI be measured in a service business with no physical inventory?

Yes, and often more directly than in product businesses. Service businesses carry their inefficiency in delivery time and owner dependency. The ROI calculation centers on three numbers: delivery cost per client engagement before and after process standardization, the change in Days Sales Outstanding after billing processes are fixed, and the owner hours recovered per week when processes are documented and team-owned. All three are measurable within the 180-day window.

How is process improvement ROI different from the ROI of buying new software or hiring?

Software and hiring add capacity. Process improvement protects margin. A new hire placed inside a broken process inherits the inefficiency and amplifies it. Software layered on an undocumented workflow produces the same broken result at higher speed. Process improvement addresses the structural cause before capacity is added. The return starts from a cleaner baseline because it reduces existing cost that is already happening, not new cost introduced in hopes that revenue follows.

The Back Office Brief

Get a weekly insight connecting back office operations to profit. Delivered every week, free.

Comments